Sales and Use Taxes

Background

State sales and use taxes were introduced in 1935 and 1937, respectively. The sales tax is a consumption tax levied on sales of tangible personal property and some services.1 The tax is paid by consumers and collected by vendors on the state’s behalf. Generally, vendors remit sales tax returns to the Colorado Department of Revenue on a monthly basis, though some vendors with very few sales may file returns either quarterly or annually. The state allows vendors with less than $1 million in taxable sales during a filing period to deduct and retain a portion of sales tax collections to offset the cost of collecting and remitting tax to the state, commonly called a vendor fee. The vendor fee is equal to 4 percent of the sales tax, but is capped at $1,000 per filing period per retailer. During 2023, the vendor fee rate was temporarily increased to 5.3 percent.

Colorado has a complementary use tax that applies when sales tax is owed but was not collected, if, for instance, the seller had not been authorized as a vendor. When personal property on which sales tax was not collected is consumed, the consumer is responsible for remitting the use tax to the state. Instructions and forms for filing use tax are available on the Department of Revenue website. Use tax revenue is largely driven by capital investment among manufacturing, energy, and mining firms.

Sales and use taxes are subject to the TABOR limit on state revenue and spending. In addition to the state sales tax, the state collects and administers sales taxes levied by counties, statutory cities, and special districts. Home rule cities are responsible for administering their own sales taxes; however, some choose to have the state collect sales tax on their behalf. Vendors are required to file a sales tax return for each business location they operate; doing so allows the Department of Revenue to distribute local sales tax revenue to the appropriate taxing district. Local sales tax revenue is not subject to the state TABOR limit, but is subject to local government TABOR limitations.

Filing frequency for use taxes depends on the type of use tax collected. Retailer’s use tax is typically filed and remitted monthly. For businesses filing consumer use tax, taxes are due depending on the amount of tax owed. For individuals filing consumer use tax, taxes are due on April 15, following the year in which sales occurred. Beginning in tax year 2015, use taxes may be reported on the state individual income tax return.

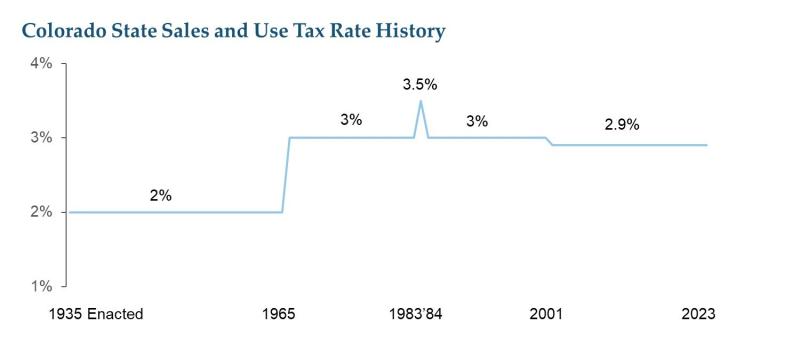

Tax Rate

Tax Exemptions

There are over 80 sales and use tax exemptions, many of which allow the state to avoid “tax pyramiding,” whereby individual products are taxed multiple times at multiple stages of the production cycle.2 Other exemptions include most food for domestic home consumption and both gasoline and diesel fuel, which are instead subject to fuel excise taxes. The Department of Revenue publishes information on sales and use tax exemptions in its biennial Tax Profile and Expenditure Report. Several of the historically large sales and use tax exemptions are listed below.

-

wholesale sales;3

-

sales of tangible personal property that becomes a component part of a manufactured product or service;4

-

sales of food for domestic home consumption;5

-

sales of gasoline and special fuel, including diesel, natural gas, propane, and kerosene;6

-

sales and purchases of livestock and live fish for stocking purposes; 7

-

sales to the United States government and the state of Colorado, its departments, institutions, and political subdivisions;8

-

sales of prescription drugs, medical equipment, and medical devices;9

-

sales of fuel for residential heat, light, and power;10

-

sales of construction and building materials used by contractors on public works projects, tax-exempt organizations, and public schools;11

-

sales of feed for livestock, seeds, and orchard trees;12 and

-

sales of machinery or machine tools used in the manufacturing process.13

Distribution

Via the Old Age Pension Fund, sales and use tax revenue is allocated to the General Fund for spending on general operations at the discretion of the General Assembly.14 In FY 2021-22, sales tax revenue totaled $4.1 billion, the second highest amount of any state tax. Use tax revenue totaled $233 million for the same fiscal year.

Federal Taxes

Sales and use taxes are not collected at the federal level.

State Comparisons

Among the 45 states that assess state sales and use taxes, Colorado’s tax rate is the lowest in the country. When comparing both state and local government sales tax rates across states, Colorado's rates are higher than the national average. California's sales tax rate is the highest in the country at 7.25 percent, while Indiana, Mississippi, Rhode Island, and Tennessee each levy 7 percent state sales taxes. Five states, including Alaska, Delaware, Montana, New Hampshire, and Oregon, do not assess sales taxes.